Averaging Down vs Dollar-Cost Averaging: Which Strategy Wins?

Both strategies involve buying more shares as prices drop — but the similarities end there. One is reactive and conviction-based; the other is systematic and emotion-free. Choosing wrong can mean the difference between recovering your losses and compounding them.

Key Takeaways

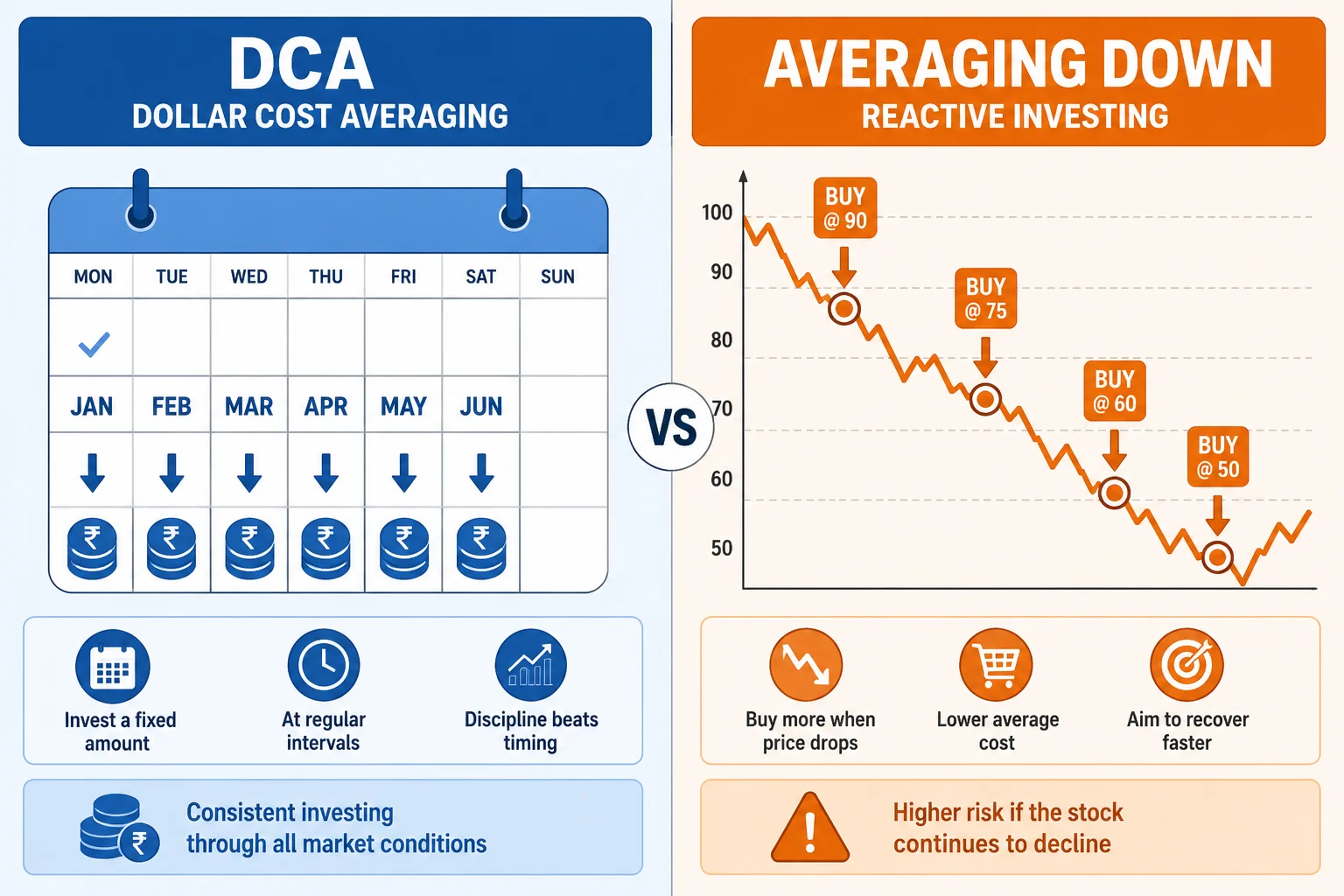

5 points- 1DCA = fixed amount invested at fixed intervals, regardless of price. Averaging Down = buying more because the price dropped.

- 2DCA works best with index funds. Averaging Down works on individual stocks — but only with fundamental conviction.

- 3Lump-sum beats DCA in 68% of historical periods — but DCA wins psychologically.

- 4Averaging down amplifies losses if the business is declining. Never average down without a fundamental check.

- 5Hybrid approach: use DCA for index funds, selective averaging down for individual high-conviction positions.

The Core Difference: Reactive vs Systematic

If you're trying to understand the difference between averaging down and dollar-cost averaging for the first time, start with the trigger. Dollar-Cost Averaging (DCA) is a time-based strategy. You invest a fixed amount (say $500/month) on the same date every month, regardless of whether the market is up, down, or sideways. The discipline is in the calendar, not the price.

Averaging Down is a price-based reaction. So what is averaging down in stocks, exactly? When a stock you already own drops below your purchase price, you buy more to lower your average cost. The trigger is the price drop, not the calendar.

| Factor | Dollar-Cost Averaging | Averaging Down |

|---|---|---|

| Trigger | Calendar date | Price drop below cost |

| Asset type | Best for index funds/ETFs | Individual stocks |

| Emotion required | None (automated) | Conviction & analysis |

| Risk of failure | Low (diversified) | High if business failing |

| Frequency | Regular (monthly/weekly) | Occasional (price-triggered) |

| Best for | Passive, long-term investors | Active, fundamental investors |

When DCA Wins

For beginners deciding whether dollar-cost averaging is better than averaging down, DCA is usually the right strategy when:

- You're investing in diversified index funds (Nifty 50, S&P 500)

- You don't have the time or interest to analyze individual companies

- You want to eliminate market-timing decisions entirely

- You have a regular income and invest monthly from your paycheck

- Your investment horizon is 10+ years

The magic of DCA: in a falling market, your fixed $500 buys more shares (lower price). In a rising market, you buy fewer shares (higher price). Over time, your average cost naturally stays below the average price — without any active decision-making.

When Averaging Down Works

Knowing when to average down on a stock comes down to four conditions — averaging down is the right move when:

- Fundamentals are unchanged: The business is still growing, the drop is market noise

- You have high conviction: You've analyzed the company and you'd be happy to own more at current prices

- Position size allows it: After averaging down, the stock is still ≤10-15% of your portfolio

- The drop is sector-wide: If the entire sector is down, not just your stock, it's often a better signal

Warning: When averaging down destroys portfolios

Averaging down on a company with: deteriorating earnings, rising debt, losing customers, or facing industry disruption is called "catching a falling knife." The stock price is reflecting a fundamental problem. More shares of a failing business means bigger losses.

Real-World Example: DCA vs Averaging Down

DCA Example: You invest ₹5,000/month in a Nifty 50 index fund for 12 months. The market falls 20% in month 3, then recovers. Your average cost is lower than if you'd invested the full ₹60,000 at the start of month 1 — you bought more units during the dip automatically.

Averaging Down Example: You buy 100 shares of Infosys at ₹1,500 (₹1,50,000 invested). The stock drops to ₹1,200 due to a market correction. You analyze the business: earnings are strong, IT spending is growing, management is solid. You buy 125 more shares at ₹1,200 (₹1,50,000 more). Your new average: ₹1,333. You now need a 11% recovery to break even instead of a 25% recovery.

The Hybrid Approach Most Investors Use

Experienced investors often combine both:

- 70-80% of portfolio: Index funds via DCA (monthly SIP)

- 20-30% of portfolio: Individual stocks, selectively averaged down when conviction is high

This gives you the safety and discipline of DCA while allowing you to take advantage of mispricings in individual stocks you've analyzed.

Use Our Calculator

Use the Stock Averager Calculator to calculate exactly how many shares to buy when averaging down, and what your new average cost will be. For DCA projections, use the SIP Calculator.

How to Calculate Your New Average Price After Averaging Down

The math is simpler than most beginners expect. Add the total amount you invested across all purchases, then divide by the total number of shares you now own. In the Infosys example above, ₹3,00,000 invested across 225 shares gives a new average cost of roughly ₹1,333. Lowering your cost basis this way reduces the percentage recovery you need to break even — but it only helps if the underlying business is still sound. Run the exact numbers with the Stock Averager Calculator and confirm your break-even target using the Break-even Calculator.

Final Verdict

Neither strategy is universally better. Use DCA for your core, diversified holdings. Use selective averaging down for your high-conviction individual stocks — but only after confirming the business fundamentals are intact. The worst outcome is averaging down on a stock with deteriorating fundamentals, which turns a temporary loss into a permanent one.

About Stock Averager Team

Expert financial analysts dedicated to simplifying complex investment strategies for everyone. We build tools that help you make better money decisions.