Delta Neutral Strategy: Profit Without Predicting Direction

What if you could make money without predicting whether a stock goes up or down? Delta neutral strategies do exactly that — they profit from volatility, time decay, or volatility changes regardless of direction. It's how professional market makers trade.

Key Takeaways

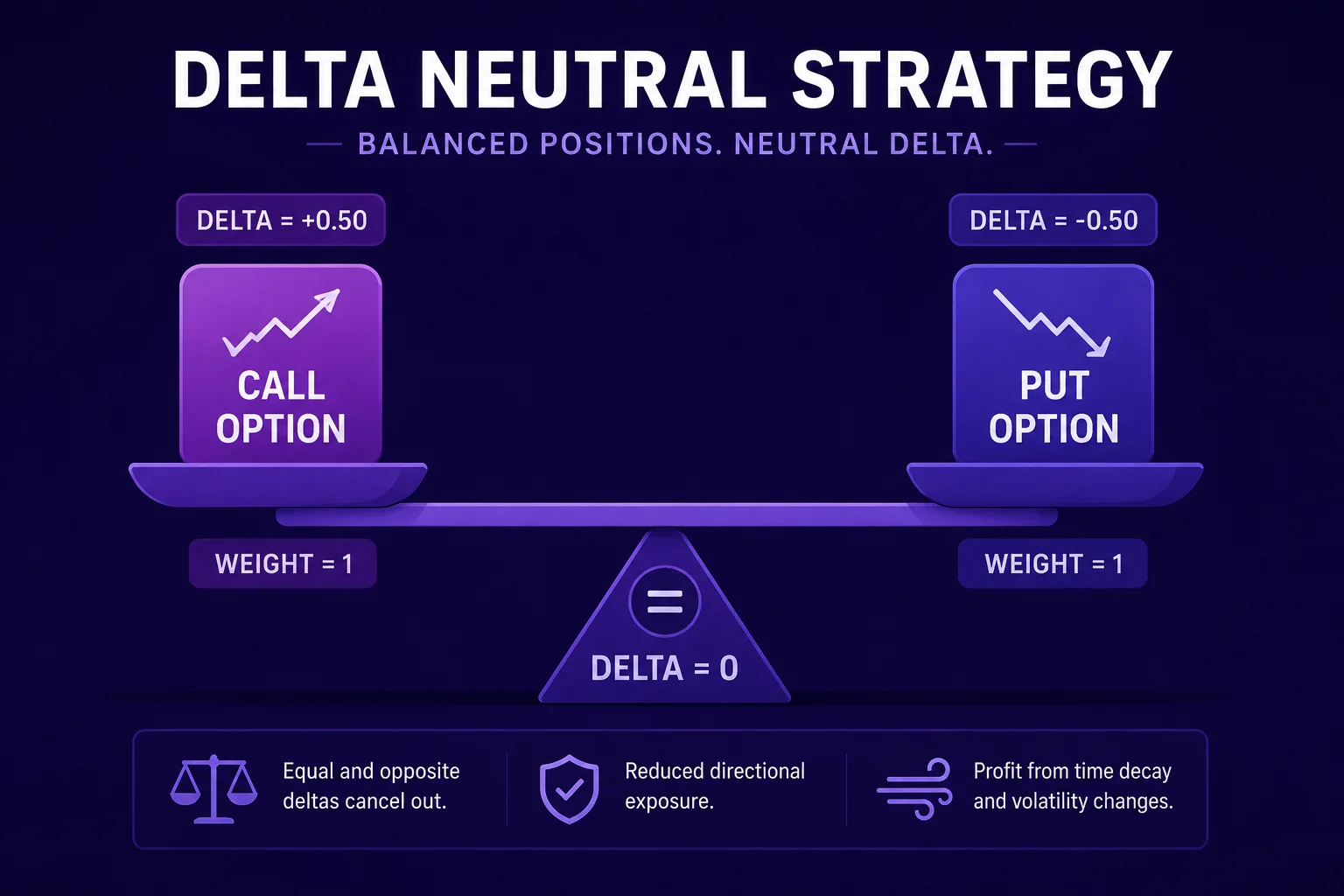

5 points- 1Delta neutral = portfolio Delta ≈ 0. Small stock moves don't affect your P&L.

- 2Used by: market makers, volatility traders, earnings traders, and advanced retail traders.

- 3Common delta neutral strategies: straddles, strangles, iron condors, calendar spreads.

- 4Profit sources: IV decay after events (short Vega), theta decay over time (short Theta), or IV expansion (long Vega).

- 5Requires active management: Delta drifts as the stock moves (due to Gamma). Requires 'Delta hedging' to maintain neutrality.

Updated for May 2026

Delta-neutral trading in the current vol regime

- • VIX has been range-bound 14-22 most of the year. That is a "mid-vol" environment — neither cheap enough for outright long premium nor expensive enough to mass-short volatility. Iron condors and short strangles with tight risk controls have outperformed bare straddles in this regime.

- • 0DTE has changed short-premium math. Daily-expiry contracts have compressed weekly IV and accelerated theta capture for short-vol traders, but they have also raised gamma risk dramatically into the close. Short straddles on 0DTE are not a beginner trade — gamma can wipe a week of theta in 30 minutes.

- • Earnings IV crush still works. The textbook "sell premium into earnings, close after the announcement" trade has remained profitable on average through 2025-26 for liquid mega-caps, but realized moves have widened — size each position smaller than the implied move suggests.

- • Use IV Rank, not absolute IV. A 35% IV today is not the same opportunity as a 35% IV two years ago. Filter every delta-neutral setup by IV Rank (or IV Percentile) on the underlying — sell premium only when IV Rank > 50, and lean long-vol when IV Rank < 20.

What Is Delta Neutral?

If you're wondering what a delta neutral strategy is in options trading for beginners, the short answer is this: a delta neutral position has a total Delta of approximately zero. This means that for small moves in the underlying stock, your profit or loss is minimal — you're not directionally exposed.

Example: You own 100 shares of a stock (Delta = +1.0 per share = +100 total). You buy 2 puts with Delta = -0.50 each (-100 total). Net Delta = 100 + (-100) = 0. The position is delta neutral.

Common Delta Neutral Strategies

Long Straddle (Positive Gamma, Positive Vega)

Buy an ATM call and ATM put at the same strike. Delta ≈ 0. Profits if the stock makes a large move in either direction, or if IV rises sharply. This is one of the most common delta neutral options strategies for earnings volatility, used by traders expecting a large move. Costs premium (Theta works against you).

Short Straddle (Negative Gamma, Negative Vega)

Sell an ATM call and ATM put. Delta ≈ 0. Profits if the stock stays near current price (theta decay) and if IV falls. Used in high-IV environments. Risk: unlimited if the stock moves sharply.

Iron Condor

Sell an OTM call spread and OTM put spread. Near-zero Delta. Profits if the stock stays within a range. Defined risk — your max loss is capped. Preferred by retail traders over naked straddles for defined risk. See our full guide: Iron Condor Strategy Guide.

Calendar Spread

Sell a near-expiry option, buy a far-expiry option at the same strike. Near-zero net Delta. Profits from time decay differential (near-expiry decays faster) and from IV expansion. A "Vega positive" theta strategy. See: Calendar Spreads Guide.

Why Delta Doesn't Stay Neutral: The Gamma Problem

A delta neutral position doesn't stay neutral. As the stock price moves, Gamma causes Delta to drift. If you're long a straddle and the stock rises $5, your call Delta increases (you're now net positive Delta — benefiting from the stock's direction). This Delta drift is why you make money on large moves with a long straddle.

For short straddles (sellers), the opposite happens: rising stock = increasing Delta (you're now short Delta — losing from the move). This is why short delta neutral positions are "Gamma scalping" territory — professionals continuously buy/sell shares to re-neutralize their Delta as it drifts. Understanding how to keep a position delta neutral as the stock moves is the single hardest part of running these trades profitably.

Practical Delta Hedging Example

You sell a short straddle: short 1 call (Delta = -0.50) and short 1 put (Delta = +0.50). Net Delta = 0. The stock rises $10. Your call Delta is now -0.65, your put Delta is +0.35. Net Delta = -0.30 (short Delta — losing on the upward move).

To re-hedge: buy 30 shares (Delta = +0.30) to bring net Delta back to 0. Then if the stock falls $10, you'd sell those 30 shares. This continuous buying low and selling high creates profit — the core of market maker strategies, and a clear, step-by-step look at how delta hedging works with a real example.

Who Uses Delta Neutral Strategies?

- Market makers: Continuously delta-hedge to extract pure volatility premium

- Earnings volatility traders: Long straddles before earnings; short straddles for IV crush

- Income traders: Iron condors and short strangles to collect theta

- Advanced retail traders: Calendar spreads for Vega exposure with managed risk

Delta Neutral vs Directional Trading: Which Should Beginners Choose?

A common question is delta neutral vs directional options trading — which is better for beginners. Directional trades (buying a call or put) are simpler to understand and only require a view on where the stock is heading. Delta neutral strategies, by contrast, remove the need to be right on direction but demand active monitoring, hedging, and a working grasp of Gamma, Theta, and Vega. For most newcomers, mastering a single defined-risk directional or income trade first — then graduating to neutral setups like iron condors — is the safer learning path.

Use the Greeks Calculator

Use our Options Greeks Calculator to calculate the total Delta of your position before entering. For multi-leg strategies, sum the Delta of each leg (positive for long calls/short puts; negative for short calls/long puts) to check if your net Delta is near zero. You can also model the full payoff in our Options Strategy Builder to see how to build a delta neutral options position step by step before risking capital.

Disclaimer

Delta neutral strategies are advanced options techniques. Selling options carries significant risk of loss. This is for educational purposes only. Paper trade before using real capital.

About Stock Averager Team

Expert financial analysts dedicated to simplifying complex investment strategies for everyone. We build tools that help you make better money decisions.