How Inflation Erodes Your SIP Returns (And What to Do About It)

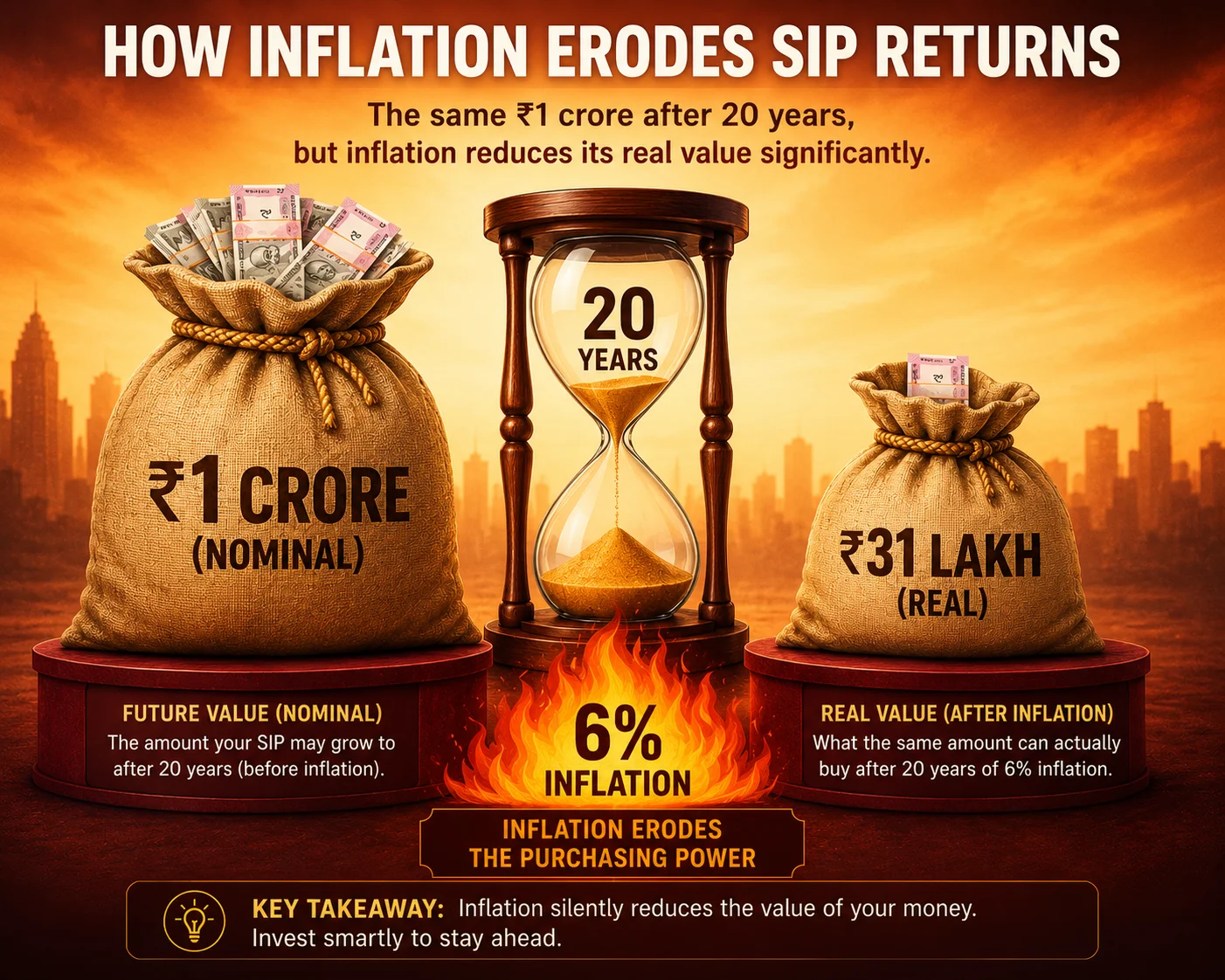

Your SIP calculator shows you'll have ₹1 crore in 20 years. What it doesn't show: at 6% inflation, that ₹1 crore will buy only ₹31 lakh worth of goods in today's money. Ignoring inflation is the most expensive mistake in long-term investing.

Key Takeaways

5 points- 1Real return = (1 + Nominal Return) ÷ (1 + Inflation) − 1. At 12% return and 6% inflation: real return ≈ 5.7%.

- 2₹1 crore in 20 years at 6% inflation = ₹31 lakh in today's purchasing power.

- 3Step-up SIP (increasing 10% annually) is the simplest way to keep pace with inflation.

- 4Goal: target REAL returns of 5-7% above inflation, not just nominal 12%.

- 5Use the SIP Calculator with a 6-7% lower 'real return' to see inflation-adjusted corpus.

The Inflation Silent Killer

A ₹50,000/month SIP for 20 years at 12% CAGR builds to approximately ₹4.7 crore. That's the number most SIP calculators show you. But ₹4.7 crore in 2045 buys what roughly ₹1.5 crore buys today (assuming 6% annual inflation). You've built real wealth, but significantly less than the nominal number suggests. Understanding how inflation affects SIP returns over the long term is the single biggest gap between what calculators promise and what your money actually buys at retirement.

How to Calculate Real SIP Returns After Inflation

If you've ever wondered how to calculate inflation-adjusted SIP returns, the real return formula is what adjusts your investment return for inflation:

Real Return Formula

Real Return = ((1 + Nominal Return) ÷ (1 + Inflation Rate)) − 1Example: 12% nominal return, 6% inflation:

Real Return = (1.12 ÷ 1.06) − 1 = 5.66%

To calculate inflation-adjusted SIP corpus: use the SIP Calculator with 5.66% instead of 12% as your return rate. The result shows what your money will be worth in today's rupees.

Inflation Rate Assumptions

| Country | Historical Avg. Inflation | Planning Rate to Use |

|---|---|---|

| India | 5.5–7% | Use 6.5% |

| USA | 2.5–4% | Use 3.5% |

| UK | 2.5–3.5% | Use 3% |

| Singapore | 1.5–3% | Use 2.5% |

Step-Up SIP: The Inflation Antidote

The most practical solution: increase your SIP amount by 10% each year — roughly matching salary growth and inflation. This is called a step-up SIP (or top-up SIP), and if you're comparing step-up SIP vs flat SIP for beating inflation, the gap compounds dramatically over a 20-year horizon.

Example impact:

- Flat SIP of ₹10,000/month for 20 years at 12%: corpus ≈ ₹99 lakh

- Step-up SIP starting ₹10,000/month, 10% annual increase, 20 years at 12%: corpus ≈ ₹1.98 crore

- That's nearly double the corpus from the same discipline — just scaling with income

The SIP Calculator supports step-up SIP calculations. Enter your annual step-up percentage to see the dramatic difference it makes over 15-20 year horizons.

What Real Returns Mean for Goal Planning

When planning for retirement or a financial goal, always think in real (inflation-adjusted) money:

- Wrong approach: "I need ₹2 crore to retire in 20 years." — This ignores inflation.

- Right approach: "I need ₹2 crore in today's rupees. At 6.5% inflation over 20 years, I actually need ₹2 crore × (1.065)^20 = ₹7.1 crore in nominal terms."

Factor in inflation to your goal amount first, then calculate the SIP needed to reach that nominal target.

Asset Classes That Beat Inflation

| Asset Class | Historical Return (India) | Real Return (after 6.5% inflation) |

|---|---|---|

| Large-cap equity (Nifty 50) | 12–13% | +5.2–6.1% |

| Mid/small-cap equity | 14–17% | +7.0–9.9% |

| Debt/bond funds | 6–8% | -0.5 to +1.4% |

| Fixed Deposit (FD) | 6–7% | -0.5 to +0.5% |

| Gold | 8–10% | +1.4–3.3% |

Only equity SIPs consistently beat inflation by a meaningful margin in the long run. Debt funds and FDs barely keep pace — in some years, they produce negative real returns. This is why understanding which investments beat inflation in India matters more than chasing the highest headline return.

Does a SIP Really Beat Inflation Over 20 Years?

Yes — but only equity SIPs do so reliably. A long-term equity SIP earning around 12% nominal against 6.5% inflation delivers a real return of roughly 5.2–6.1%, meaning your purchasing power genuinely grows year after year. The longer your horizon, the more this gap compounds in your favour, which is exactly why SIP investing for beginners is best framed as a multi-decade habit rather than a short-term bet. Just remember that the corpus shown by any calculator is a nominal figure: to know the true outcome, always re-run the numbers using a real return rate. Pairing this with a CAGR Calculator helps you sanity-check whether your fund's historical returns can realistically outpace inflation.

Calculate Your Inflation-Adjusted SIP

Use our SIP Calculator to see both nominal and inflation-adjusted results. For the most accurate planning, enter your real return rate (nominal return minus inflation) to see what your future corpus is actually worth in today's rupees.

About Stock Averager Team

Expert financial analysts dedicated to simplifying complex investment strategies for everyone. We build tools that help you make better money decisions.