Vega in Options: Why Your Option Lost Money Despite Being Right

Stock moved exactly as you predicted. Your option still lost money. That's Vega — implied volatility dropped and crushed your premium even before time decay had a chance. Understanding Vega is the difference between being right on direction and being right on the trade.

Key Takeaways

5 points- 1Vega measures how much option price changes per 1% change in implied volatility (IV).

- 2Long options (buyers) have positive Vega — they benefit from rising IV.

- 3Short options (sellers) have negative Vega — they benefit from falling IV.

- 4IV crush after earnings destroys option value even when the stock moves your way.

- 5ATM options with longer expiry have the highest Vega. OTM options near expiry have nearly zero Vega.

What Is Vega?

If you've ever wondered what Vega is in options trading for beginners, here's the simplest definition: Vega (ν) measures how much an option's price changes for every 1% change in implied volatility (IV). It's not a Greek letter — it's actually a made-up term used by traders (the actual Greek letter is kappa), but Vega is universally used.

Example: An option with Vega = 0.15 gains $0.15 (or ₹0.15) for every 1% increase in IV. If IV rises from 30% to 35% (5% increase), the option gains 5 × $0.15 = $0.75, even if nothing else changes.

Why Implied Volatility Changes

Implied volatility (IV) reflects the market's expectation of future price movement. It rises when:

- Earnings are approaching (uncertainty increases)

- Major economic events are scheduled (Fed meetings, CPI data)

- The market is falling (fear increases)

- A company faces unexpected news (M&A rumors, product launches)

IV falls (crushes) when:

- The event passes (earnings announcement is made)

- Markets recover and fear recedes

- Time passes without any major news

IV Crush: The Vega Trap Investors Fall Into

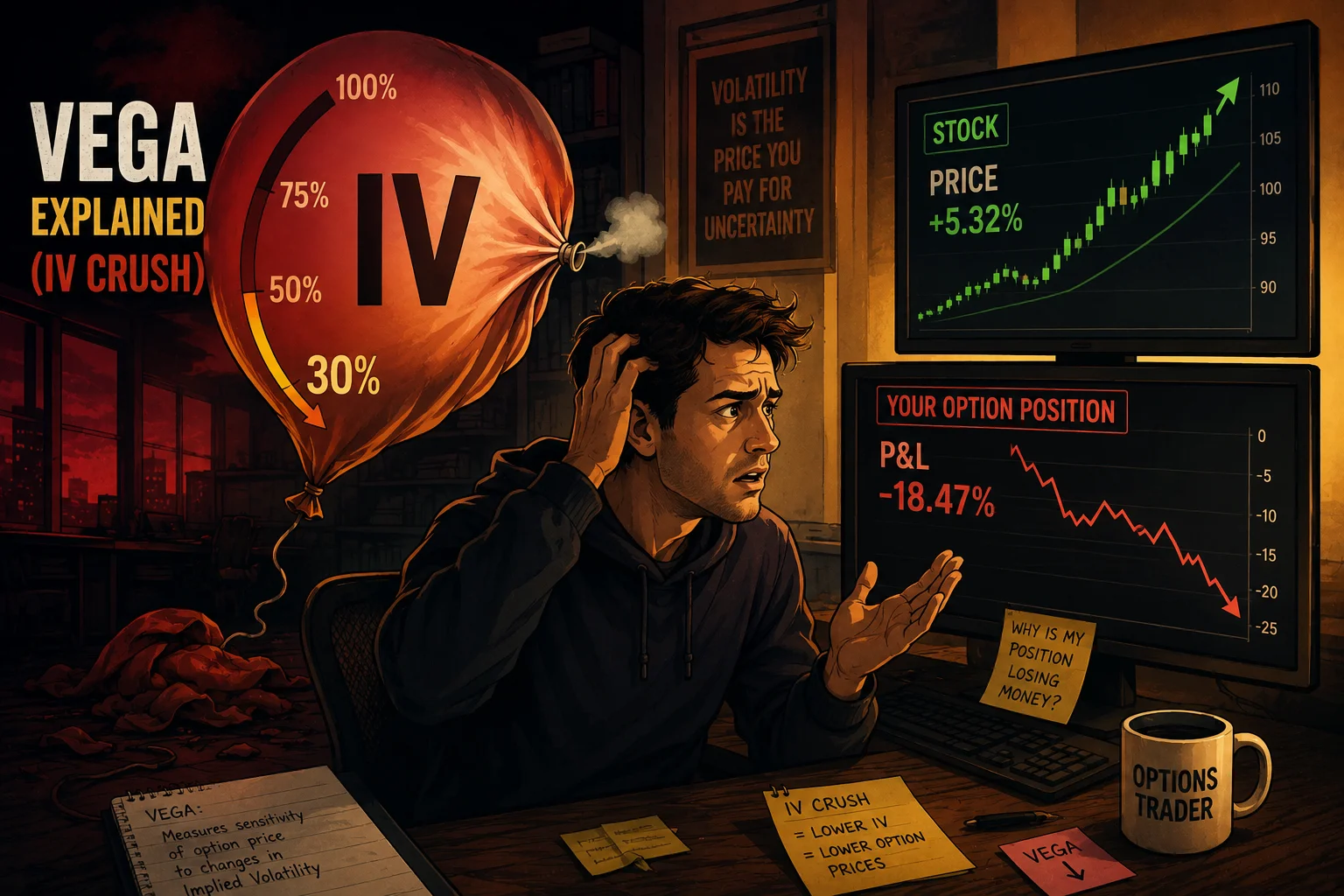

The classic Vega mistake — and the reason why your option lost money when the stock went up — is buying a call option before earnings because you're confident the stock will beat expectations. The stock goes up 5% — but your option loses value anyway.

Here's what happened: IV was 80% before earnings (high uncertainty premium). After earnings (even with a positive surprise), IV collapses to 35%. Your Vega loss (-45 IV points × Vega) outweighed your Delta gain.

This is IV crush — and it explains how implied volatility affects option prices more powerfully than most beginners expect, happening to virtually every option holder through earnings announcements. See our detailed guide: IV Crush Explained.

The Pre-Earnings Trap

IV before a major earnings = 80-120%. After earnings = 30-40%. This 50-80 point IV drop destroys 30-70% of option value immediately after the announcement, regardless of direction. Never buy options right before earnings unless you have a specific volatility strategy.

Positive vs Negative Vega

| Position | Vega Sign | Benefits From | Hurt By |

|---|---|---|---|

| Long call / long put (buyers) | Positive (+) | Rising IV | IV crush |

| Short call / short put (sellers) | Negative (−) | Falling IV | IV spikes |

| Credit spread | Negative (small) | Falling IV | IV spikes |

| Long straddle/strangle | Positive (high) | Any sharp IV move | Stable low IV |

How to Use Vega in Your Trading

- Check IV Rank before buying: Knowing how to use Vega when buying options starts here — IV Rank 30-50% = normal, 70%+ = elevated. Buying when IV rank is above 70% increases your Vega risk — you're overpaying for options.

- Sell when IV rank is high: Selling options with high IV rank means you collect inflated premiums. When IV reverts to normal, your short position profits from the Vega effect.

- Use the Volatility Impact Calculator: Our IV Impact Calculator shows exactly how your P&L changes at different IV levels.

- Calendar spreads for Vega plays: Long a far-expiry option (high Vega), short a near-expiry option (low Vega). Profits when IV rises. The "volatility trade."

Vega vs Theta: What's the Difference for Option Buyers?

Beginners often confuse the two, so here's the difference between Vega and Theta in plain terms. Theta is the steady cost of time decay — your option loses a fixed slice of value every day regardless of what volatility does. Vega is the volatility-driven swing — your option gains or loses value when implied volatility itself moves up or down.

For an option buyer, the two often work together against you: Theta bleeds value daily while a post-event IV crush erases premium all at once. That combination is why so many directionally correct trades still lose. You can see both forces side by side on your own position with the Options Greeks Calculator.

Calculate Vega on Your Position

Use our Options Greeks Calculator to see the exact Vega of any option. A Vega of 0.20 means a 5% IV rise adds $1.00 to your option's value (or costs $1.00 if short). Plan your trades knowing this number.

About Stock Averager Team

Expert financial analysts dedicated to simplifying complex investment strategies for everyone. We build tools that help you make better money decisions.