Gamma in Options: The Hidden Risk That Surprises Traders

Delta tells you where you are. Gamma tells you how fast you're moving. Ignoring Gamma in options trading is like driving without knowing your acceleration — you'll be surprised by how fast your risk changes.

Key Takeaways

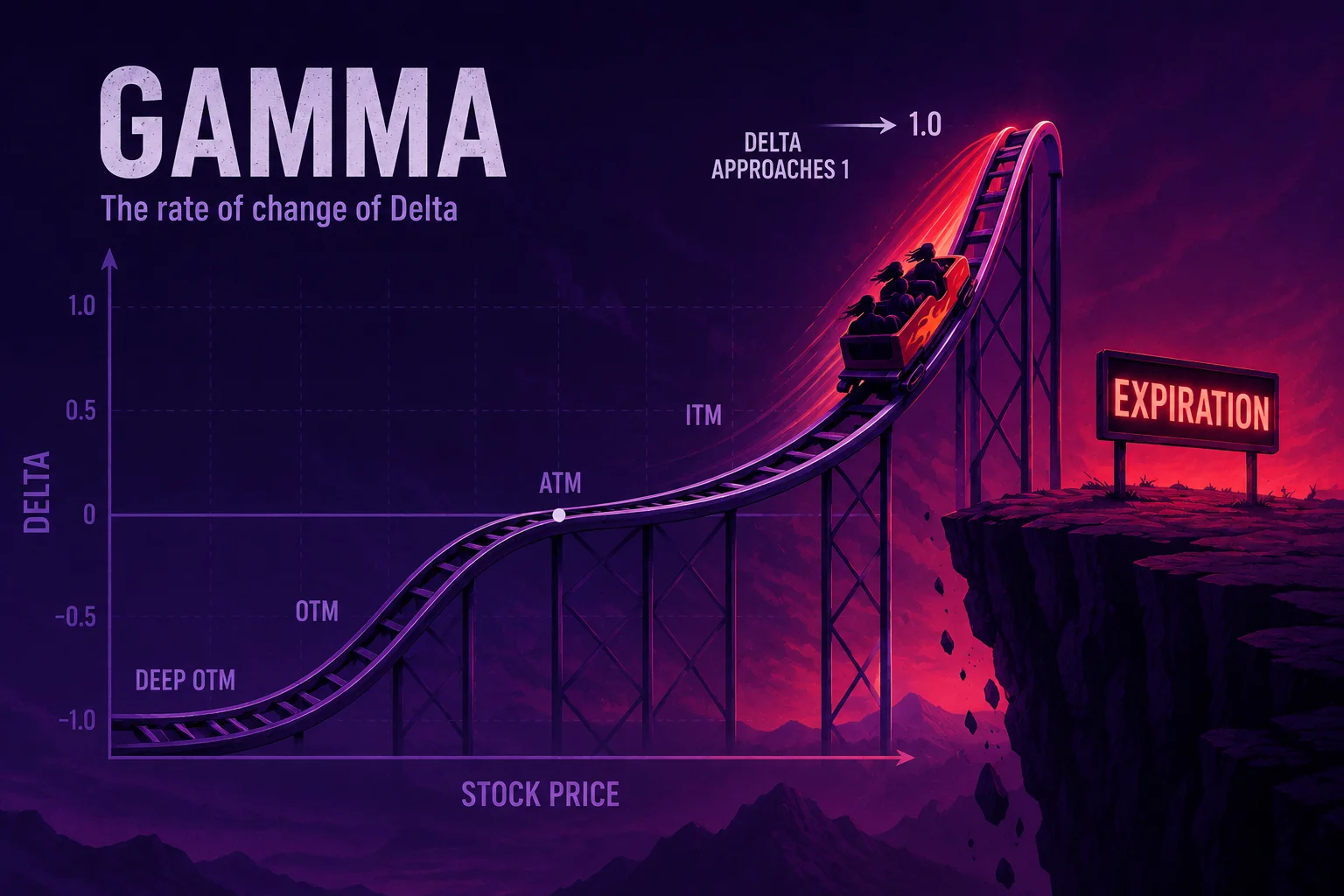

5 points- 1Gamma measures how fast Delta changes per $1 move in the underlying stock.

- 2High Gamma = Delta changes rapidly = position gets riskier faster. Dangerous near expiry.

- 3ATM options have the highest Gamma. Deep ITM and OTM options have low Gamma.

- 4Short options positions have negative Gamma — you lose money if the stock moves sharply in either direction.

- 5Gamma risk is highest in the last 7-14 days before expiration (0DTE options are extreme Gamma risk).

What Is Gamma in Options Trading?

If you have ever searched for what is Gamma in options trading for beginners, here is the simplest definition: Gamma (Γ) is the second derivative of option price — it measures how much Delta changes when the underlying moves by $1. If Delta is your speed, Gamma is your acceleration.

Example: A call option has Delta = 0.50 and Gamma = 0.05. If the stock rises $1, the new Delta = 0.50 + 0.05 = 0.55. If it rises another $1, Delta = 0.55 + 0.05 = 0.60 (approximately, since Gamma itself changes too).

Key Relationship

New Delta ≈ Old Delta + (Gamma × Stock Price Change)This is an approximation — Gamma itself changes as the stock moves. But it's accurate for small price movements.

Where Gamma Is Highest on the Options Chain

Knowing which options have the highest Gamma is the key to anticipating how quickly your risk can change. The pattern below shows how Gamma behaves across strikes and time to expiry.

| Option Type | Gamma Level | Why |

|---|---|---|

| ATM, near expiry | Highest | Small moves flip the option ITM/OTM dramatically |

| ATM, far from expiry | Moderate | More time softens the impact of moves |

| Deep ITM | Low | Delta already near 1 — small changes don't matter much |

| Deep OTM | Low | Delta near 0 — option is unlikely to be affected by small moves |

Long vs Short Gamma: What Is the Difference?

The difference between long Gamma and short Gamma comes down to whether you bought or sold the option, and it decides whether sharp moves help or hurt you.

Long Gamma (option buyers): Your position benefits from large moves in either direction. A big stock move increases your Delta rapidly — your P&L accelerates. Buyers love Gamma because they profit from volatility. The cost: you pay Theta daily.

Short Gamma (option sellers): Large moves hurt you. If the stock surges, your short call Delta increases rapidly (you're losing more than expected). If it crashes, your short put Delta becomes more negative. Sellers collect Theta but hate Gamma.

The Theta-Gamma Trade-Off

Option sellers profit from Theta (time decay) but suffer from Gamma (large moves). This is the core risk-reward of options selling. ATM options near expiry have the highest Theta AND highest Gamma — maximum income but maximum risk if the stock moves sharply.

Gamma Risk in the Final Days (0DTE)

If you are wondering why Gamma risk is highest near expiration, zero-days-to-expiry (0DTE) options are the clearest example of an extreme Gamma environment. Because there's no time value left, even small stock moves can flip an option from worthless to highly valuable (or vice versa) within minutes. 0DTE trading is popular for day traders but carries extreme Gamma risk — your position can go from profitable to max loss very fast.

How to Manage Gamma Risk

- Use spreads: Buying and selling options at different strikes reduces net Gamma exposure. A credit spread has less Gamma than a naked short option.

- Avoid selling ATM options near expiry: This is maximum Gamma risk. The preferred selling zone is 30-45 DTE where Gamma is manageable.

- Close positions at 50% profit: Taking profits early eliminates Gamma risk on the remaining days.

- Use the Greeks Calculator: Before entering any trade, check Gamma alongside Theta. High Theta with manageable Gamma is the sweet spot for sellers. You can also stress-test the trade in our Options Profit Calculator to see how the P&L curve bends as the stock moves.

Gamma vs Delta: What Is the Difference?

Beginners often ask about the difference between Gamma and Delta in options, and the distinction is simple once you frame it as motion. Delta tells you how much an option's price changes for a $1 move in the stock — it's your current speed. Gamma tells you how much that Delta itself changes for the same $1 move — it's your acceleration. A position can have a comfortable Delta today, but a high Gamma means that Delta (and your risk) can change dramatically after a single sharp move. That is why traders watch both numbers together rather than Delta alone.

Calculate Gamma on Your Position

Use our Options Greeks Calculator to calculate the exact Gamma (along with Delta, Theta, and Vega) for any option. Enter your strike, expiry, underlying price, and IV to see all Greeks instantly.

About Stock Averager Team

Expert financial analysts dedicated to simplifying complex investment strategies for everyone. We build tools that help you make better money decisions.